Executives must prepare for the end of the click

If your growth model still depends on paying for search, you’ll soon be out of luck.

Executives must prepare for the end of the click (H2)

In May 2024, Google CEO Sundar Pichai announced AI Overviews (AIOs), a feature where instead of showing a list of links, Google would answer queries directly using AI.

For brands, that practical little feature has had a tectonic impact on search traffic.

The numbers are staggering. Just after launch, Gartner predicted that by 2026, AIOs will depress traditional search engine volume by 25%. A widely cited Seer Interactive report found year-on-year organic click-through rates (CTRs) – even if a brand appears in results – have recently collapsed by as much as 49% (even 54% for paid).

These figures may reflect the extremes. But independently, several CMOs confirmed to me that their search traffic is down sharply — and maintaining it now costs significantly more than it did two years ago.

Google Is Becoming the Destination (h2)

As ChatGPT, Perplexity and the like are eating into search, Google is doing everything it can to keep users inside its own interface.

With AI Overviews, the platform is moving from a traffic distributor to an active intermediary that captures attention, shapes decisions, and monetises both. Brands are no longer just competing with other brands. They are competing with the interface itself.

For two decades, marketers treated Google like a demand vending machine: insert budget, select keywords, receive customers. We built an entire profession around tweaking websites and keywords, so that brands show on Google page one.

Search marketing worked because of an implicit agreement: Google passes people on.

That agreement has now been cancelled – and it’s just a preview of what comes next.

Increasingly, AI agents can make purchasing decisions on behalf of humans. The platforms will no longer just be intermediaries. They could turn into buyers.

Marketers are again flocking to optimise for this. Generative Engine Optimisation (GEO) trainings are full. Sure, GEO is a no-regret move. But growth from such optimising still rests on one assumption, that in the future, platforms will still send customers your way.

They might do, but equally, they might not.

Brands and Relationships (h3)

As optimising auctions becomes harder, strong brands and direct customer relationships will decide the winners.

People search “Porsche”, not “fast car”. “Swiffer”, not “disposable duster”. “PlayStation”, not “computer game”. If customers look for your brand instead of the category, you have already won half the battle.

Where does the AI learn what the customer prefers? From the human’s past behaviour. If your brand is already preferred, the machine learns that preference and acts on it. If your brand is unknown, the machine sorts by price and availability. You become a commodity by default.

For years, marketers have shifted budgets away from brand building into so called “performance marketing”. It was easier to do that traditional campaigning, as it was quick and promised easy returns. Many of us have pointed out that imbalance. Now the bill arrives.

Strong brands survive platform shifts; weak brands probably won’t. In a world where you can’t reliably pay platforms to send customers your way, a strong brand will remain the best insurance policy.

A good image and salience aren’t enough. Strong brands build preference — the third step in the funnel after awareness and consideration. Preference is what makes someone ask for you by name, before they even check out alternatives. You can’t buy that. You can’t GEO-optimise your way to it. Building preference requires the full 4Ps marketing toolkit — as well as insight, creativity, and consistency.

There’s another path to thrive outside the platforms and that’s direct customer relationships. Not attribution models, not dashboards — actual connections. Be that email lists, loyalty programs, apps, user groups, subscriptions. Every direct relationship you own has compounding value.

From L’Oréal to Air France to Adobe, brands worldwide have made the shift to direct relationships. It won’t work for all categories. B2B or service brands will, admittedly, find this easier.

And building customer relationships is much more work than paying a platform to send people to you. You have to earn the opt-in. But the return is a feedback loop and an audience no platform can take away.

A refocus on brands and relationships doesn’t mean abandoning Google. To the contrary. To build brand preference and relationships, marketers must deploy the most effective channels — online and offline — including social, AI agents, YouTube, TV, and more.

For strong brands, the switch will be easier. For weaker ones, it means surviving the search drop while building brand strength and relationships simultaneously. That’s harder. But it’s the only switch worth making.

The click is fading. Strong brands and customer connections scale. They always have.

CEOs should stop mistaking their opinions for the market

Corporate leaders increasingly claim they are speaking for the market. In reality, they are often speaking for themselves.

When Unilever CEO Fernando Fernandez recently told investors that traditional advertising is essentially dead — and that the company will pivot toward creators and influencers — the reaction ranged from disbelief to ridicule.

It reminded me of former Adidas CEO Kasper Rørsted going on television and declaring that Adidas would move its marketing almost entirely into digital. The company later quietly reversed course after growth slowed.

Both tried to sound cool. Both ignored science and evidence. Fortunately, customers didn’t care.

They do care when CEOs drag their companies into political debates, though.

When Salesforce CEO Marc Benioff suggested deploying the National Guard to address crime in San Francisco, some customers walked out. Elon Musk’s political interventions have repeatedly dragged Tesla into controversies and alienated customer groups (but then, that’s what Musk does).

Marketing is hardly immune.

Over the past decade marketers have repeatedly tried to turn brands into moral actors. Gillette’s ‘The Best Men Can Be’ campaign. Unilever’s multi-year push to give mayonnaise a social purpose. Brands contorting themselves around DEI debates they were never equipped to lead.

Many of these public moves angered parts of the customer base. Most quietly disappeared because they had little impact.

Different industries. Different issues. The same pattern. A leader expresses a personal belief. Suddenly the company finds itself defending a position it never formally chose.

The underlying problem is simple. Leaders — including marketers — too often assume their own views represent the market. They don’t.

Why companies are stepping into controversies

In new research for Harvard Business Review involving more than 1,000 senior executives — including CEOs and CMOs — Kimberly Whitler and I examined who actually pressures leaders to take controversial public positions.

Most people assume the pressure comes from outside: customers, media, activists, investors, or social media outrage. It doesn’t. Strong pressure comes from inside the company — and from leaders themselves.

Most executives will tell you they act because it’s what customers want. In reality, many simply assume that’s what customers want.

Leaders’ own beliefs, colleagues, and internal departments such as DEI and CSR are almost as influential as customers themselves. Customers scored higher. But they were only one voice among many.

This matters because CEOs are not the customer. Marketers are not the customer. Most belong to a remarkably narrow demographic: educated, urban professionals surrounded by colleagues with similar backgrounds, education and political views. Their customers look nothing like that. They are older and younger, richer and poorer — mostly the latter — conservative and progressive, and largely indifferent to the internal debates of the brands they buy from.

The danger is obvious. Executives hear the loudest voices inside the building and mistake those voices for the market.

This is where marketing should step up. Marketing does not exist to echo internal opinion. Marketing exists to drive growth, understand customers, and to represent them inside the organisation.

That means bringing evidence into internal debates. Testing assumptions. Showing how customers actually think rather than accepting how executives assume they think.

Marketers must become better advisers to their CEOs. Because when companies enter public debates, the question should never be: what do we believe? The real question is harder. What do customers actually believe?

The leadership case for pausing ad spend

The New Zealand retailer’s decision to pause ad spend for eight weeks isn’t the cavalier move some say, but an A/B test all marketers should follow closely.

In the fast-moving retail category, eight weeks is an eternity. Especially if the CMO of a retail brand pauses all search, social and TV spending to see and learn from what happens.

A few days into the job, the new marketing officer of New Zealand’s The Warehouse, Frankie Coulter, shocked many by announcing an eight-week pause on all external advertising. Only internal in-store media and promotions will continue. This isn’t budget trimming. It’s a deliberate, large-scale A/B test to measure the real effect of external advertising on the business — and to determine the most effective media mix.

The move is risky. Retail is unforgiving. Margins are thin. Performance is judged weekly. Agencies, platforms (and less marketing-savvy executives) are holding their breath. What if the result shows the business can spend less? At the same time, some applauded the move. Finally, someone prepared to challenge media orthodoxy rather than optimise within it was the sentiment from the cheerleaders.

Only internal in-store media and promotions will continue. This isn’t budget trimming. It’s a deliberate, large-scale A/B test to measure the real effect of external advertising on the business — and to determine the most effective media mix.

The move is risky. Retail is unforgiving. Margins are thin. Performance is judged weekly. Agencies, platforms (and less marketing-savvy executives) are holding their breath. What if the result shows the business can spend less? At the same time, some applauded the move. Finally, someone prepared to challenge media orthodoxy rather than optimise within it was the sentiment from the cheerleaders.

The Warehouse is New Zealand’s largest retailer — the local equivalent of Tesco or Walmart. It employs more than 10,000 staff and has outlets in every corner of the country — and New Zealand has many corners. It commands a significant chunk of national advertising spend.

But the company is under pressure. Significant losses have led to restructuring with 270 roles recently cut. It’s a case of a brand in need of a turnaround.

It’s a predominantly bricks-and-mortar business, with just 7% of its sales coming online. Yet, the firm has been throwing millions at search, social and other digital media—largely because everyone else does. After all, no marketer ever got fired for doing the same as the competition. But it has neglected its most powerful channels: retail media and local store activity.

We all know what easy marketing money creates. The Association of National Advertisers (ANA) has repeatedly warned that a significant share of digital media investment fails to reach intended audiences. Companies like Procter & Gamble and Unilever have publicly laid out initiatives to tighten the effectiveness of their mix, much of which is digital, after scrutinising effectiveness. Yet digital expenditure continues to rise.

Coulter wasn’t hired to preserve the status quo. It was clear something had to change. This isn’t an anti-digital crusade. It’s not a rejection of Google or Facebook. The objective is balance—learn what works, so the company can spend where it genuinely moves the needle.

In his own words: ‘I don’t like spending money unless I understand the value I’m getting for that money.’

Before anyone dismisses this as bravado, Frankie Coulter knows what he’s doing. His 25+ years’ experience spans senior roles at Kraft Heinz, Kellogg’s, Dr Scholl’s and Boots. He has been repeatedly recognised among the country’s best marketers. He’s a Fellow of The Marketing Academy. Coulter understands brands. He understands business. And he understands risk. Most importantly, what Coulter understands is measurement reality.

Marketing returns are far harder to figure out than most people claim. Even for AI, there are just too many variables: message, audience, creative execution, budget, medium, time of day, time of year, distribution, competitive pressure. I’ve built and interrogated many models myself at McKinsey and with CMOs. Trust me, if you talk “full market mix”, even the best rarely explain half of performance; 70% would be extraordinary.

Which is why serious marketers rely on something more fundamental: A/B tests. Marketing isn’t a belief system. People learn through controlled experiments. Adjust price. Change creative. Shift channel mix. Observe. Learn. Repeat. Procter & Gamble and Unilever built marketing powerhouses on exactly this testing discipline. Back in 2017, P&G cut more than $200m in digital spend to test its impact and saw little effect on sales. Adidas leaned heavily into digital before rebalancing when growth faltered. These were not ideological shifts. They were A/B tests. Pausing spend to measure impact is not careless. It is rigorous.

Coulter’s test won’t resolve every question, particularly long-term brand impact. Eight weeks is too short for that. But in short-cycle retail, it will provide a clear read on footfall and revenue. By reintroducing channels one by one, the team can observe incremental impact directly rather than infer it from imperfect attribution models.

At conferences, marketers talk endlessly about bold moves. But at home, few challenge how budgets are allocated. Fewer still are willing to risk testing which part of their spend may be unnecessary. But everyone will and should watch this A/B test closely.

We need more marketers who dare to question their marketing effectiveness, including pausing spend. That’s not recklessness. That’s marketing leadership.

Podcast: Why marketers struggle in the boardroom

Thomas shares practical tactics for building stronger CFO relationships, acting with more bravery, and avoiding the “safe” behaviours that quietly kill careers. A must-listen for any marketer serious about leadership.

You can listen to the podcast here.

A New Year’s wish: let’s ditch brand marketing

Performance marketing has an evil twin: brand marketing – another term that promises clarity, but mostly delivers the opposite

Just before Christmas, I wrote a column arguing that performance marketing should be retired. It’s a misleading label for direct response marketing that delivers mostly confusion – particularly in boardrooms increasingly anxious about short-term results.

The response was immediate and broad. Hundreds of messages from marketers around the world agreed. ‘Direct response’ it is. But almost immediately, another pattern emerged.

Many replies pivoted not to language, but to budgets. ‘We should spend more on brand.’ ‘My brand team says the same.’

It seems performance marketing didn’t arrive alone. It acquired an evil twin: brand marketing. Two labels, supposedly describing opposite ends of the spectrum, both promising clarity. And yet both managing to make the job harder.

What’s particularly curious is how ‘brand marketing’ has come to mean something very specific. Not the cumulative effect of products, prices, services and experiences. But a role. A budget. In some organisations, people are hired explicitly to ‘do brand’, often with little influence over the things that actually shape it.

I should explain where my confusion comes from. I grew up in the FMCG sector. Heavy TV, outdoor, print – and plenty of direct response. My global team had a very simple job: ship boxes. We measured short-term results relentlessly. We also tracked brand health over time. But we never treated these as separate worlds.

The first time I encountered a hard separation was when telecoms and pharma companies tried to recruit me to build so-called ‘brand teams’. On paper, it sounded strategic. In practice, it was baffling. ‘Brand’ meant advertising. Full stop. Not product. Not pricing. Not service or distribution. Just decks, frameworks and campaigns. When I asked how a brand could be built without touching product, price or place, the conversation tended to stop.

This isolated brand thinking has now become widespread. Today, at conferences, I commonly meet marketers working in ‘brand’ departments, far removed from commercial decisions, producing elaborate positioning frameworks while lamenting that their company doesn’t spend ‘60% on brand’. That’s a generalisation. But it’s a familiar one.

It’s worth pausing to restate some brand building basics:

Every marketing activity builds the brand.

Customers don’t experience marketing in silos. They don’t distinguish between a TV ad, a price increase, a frustrating call-centre interaction, a broken product, a Facebook coupon or a confusing offer. It all blends into a single view of the brand.

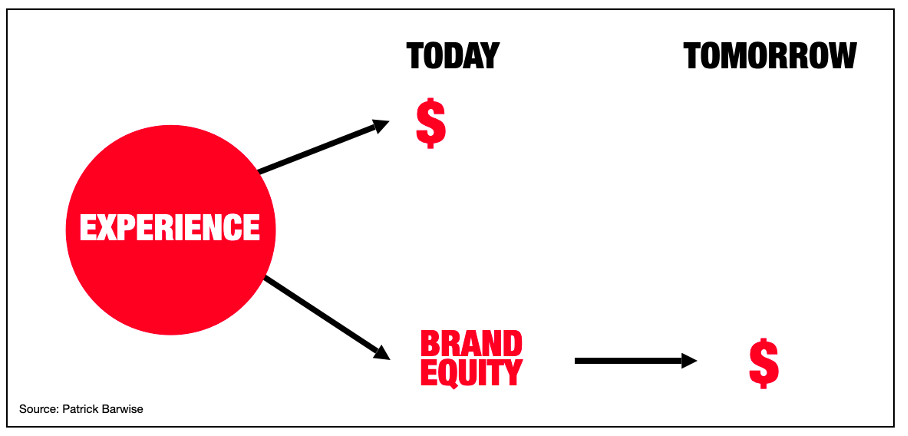

Professor Patrick Barwise, former head of London Business School’s marketing department, showed this neatly years ago:

Every customer experience creates a short-term financial effect. You typically spend money. That’s a cost. The customer may or may not respond and generate revenue.

Effective long-term brand building sells in the short term.

That same experience also creates a memory. A good one. A bad one. A memory of your product, your price, your service, your advertising. Over time, this brand equity may translate into revenue. Brand building does result from the sum of everything a customer experiences.

Millions of viewers have shed a tear this year watching Waitrose’s ‘The Perfect Gift’ Christmas ad. It was long and expensive, and it contained virtually no product promotion. System1 scored it with a 2.5-star long-term effectiveness uplift versus the supermarket category. But for Waitrose, ‘winning Christmas’ is not about winning prizes. It is about winning Christmas revenue – this year.

This is where The Long and the Short of It, by Les Binet and Peter Field, is often invoked – and rarely read properly. Drawing on hundreds of campaigns from the IPA Databank, the authors examined short-term activation and longer-term brand campaigns (as far as that distinction can realistically be made).

What they found is frequently glossed over: the campaigns that deliver the strongest long-term effects also produce the strongest short-term results. Binet and Field call them ‘brand response’ campaigns. They work immediately and they work over time. This is uncontroversial in FMCG. It is far less comfortable for organisations built around separating short and long into different teams.

The category determines how brand building works.

Binet and Field made another important observation: campaigns with roughly a 60/40 split between brand building and activation tended to perform well over time. It’s the figure most people cite today. What most people ignore is that 60/40 is an observed average, not a rule. The authors are clear that the balance varies by category.

That matters because the IPA Databank leans heavily toward consumer goods and services. Categories with long purchase cycles – durables, capital goods and many B2B markets – are thinly represented.

And categories behave very differently. Luxury handbags operate with long cycles and high emotional investment. Very few buyers are in market at any one time. Heavy activation would be wasteful and do little to build the aspiration the brand needs.

Kitchen towel is different. Low involvement. Frequent purchase. Winning at the checkout matters. Activation is king.

The mechanical application of 60/40 to all categories is difficult to justify.

Brand building doesn’t equal campaigns.

Trader Joe’s goes from strength to strength. The US retailer has a clear positioning, fierce loyalty and strong economics – without classic brand campaigns.

What customers experience instead is a coherent system: the store, the assortment, the pricing, the packaging and the people at the checkout. Promotions exist. Activation exists. And all of it builds the brand.

Brand building isn’t always synonymous with big above-the-line budgets. In fact, some of the world’s strongest brands run little or no brand advertising. The mistake is turning one executional approach into an organisational doctrine.

The neat separation of activation and brand building looks tidy on slides. Less so in the real world, where customers stubbornly refuse to experience brands in departmental chunks.

There is, of course, a role for some brand-focused work in large organisations: consistency, efficient central campaign platforms and measurement. Scale helps here. These things matter.

But treating ‘brand’ as a separate discipline never really did.

* * *

When organisations build two separate silos – one for ‘short-term activation’ and one for ‘brand’ – and blindly push a 60/40 split, it’s worth pausing. In many cases, it creates exactly the frustration it was meant to solve.

A more useful lens is the one supported by evidence, not ideology. This leads to two questions that actually matter. How does profitable brand response get built in your category? And what does that imply for how you allocate tasks and budgets?

In B2B, brand response may mean communicating the positioning while creating leads. In FMCG, it may mean shipping boxes and building the brand through consistent execution. Elsewhere, it may mean experience over advertising.

Search, coupons, TV, product and pricing – people only experience one brand. That’s why every marketer is a brand builder.

Once you accept that, the idea of ‘brand marketing’ starts to look less like a discipline and more like a misunderstanding.

All I want for Christmas is for ‘performance marketing’ to vanish

Two small words can do big damage. ‘Performance marketing’ gives marketers and C-suites the wrong idea about return on investment and needs to be retired.

Somewhere during the digital gold rush, a new term crept into the profession: performance marketing. No one knows exactly who coined it. Probably not a serious marketer or an academic. Some people point to Google. Some to a digital agency. One day we may find out.

But there’s one thing we know for sure: the term ‘performance marketing’ has caused more damage to a profession that already struggles with being taken seriously by the C-suite. That’s no small feat, given the competitive set includes ‘growth hacking’, ‘full-stack marketer’, ‘storytelling’ and ‘the metaverse’.

Meta’s CMO Alex Schultz hit the nail on its head, speaking to Marketing Week last week: “There is no such thing as performance marketing. All marketing performs.” When platforms have to explain Marketing 101 back to marketers, something has gone badly wrong.

Today, whole generations of marketers use the term in job ads, job titles and boardroom decks. Inside organisations, it spreads like gospel.

The idea of performance marketing was well intended. A label for pay-for-performance. Money moves only when something happens. A click. A lead. A sale. Paying for outcomes sounds sensible. It’s what we do in restaurants. We pay after the meal. I suppose that makes it performance dining.

But performance marketing overpromises, underdelivers and confuses many of marketing’s most important stakeholders. ‘It’s demoralising’: Meta’s CMO on retiring the term ‘performance marketing’

Here’s my list of the top reasons why:

The problems with ‘performance’

First, the obvious. Performance marketing implies – quietly but powerfully – that other marketing does not perform. People think in binaries. Above-the-line and below-the-line. Short-term and long-term. Brand and activation. Now performance and… what exactly? Non-performance? To quote Meta’s Schulz once more: “It’s just demoralising to call one performance and one brand.” Once you introduce ‘marketing that performs’, you automatically create marketing that doesn’t. That implication insults the entire discipline.

Second, performance marketing doesn’t always perform. It creates the illusion that you only pay for results. But those ‘results’ often mean clicks or click-through rates. Vanity metrics. And everybody knows: a quick search for ‘ad fraud’ shows how easily those numbers get inflated by bots. Compare click data in a social campaign with the traffic that actually lands on your site. The gap tells its own story. This isn’t an attack on digital media. Digital is powerful. Let’s just stay honest.

Third, the term accelerates corporate short-termism. For quick-win-hunting C-suites, performance marketing sounds like a lever you can pull on demand. Buy success. Soothe the quarter. Once learned, the habit sticks. Meta, Google and co reinforce the belief. Automation promises to ‘do the marketing for you’. CFOs love the idea. Why wouldn’t they? It sounds measurable, controllable and safe.

Fourth, the term quietly undermines long-term brand building. I just came back from a long tour of conference talks and university lectures. In the breaks, from Chicago to Tokyo, the same debate. How to convince CEOs that long-term brand building matters? Here’s the irony. The same marketers who pitch ‘safe’ performance budgets today are often the ones emailing CEOs Les Binet and Peter Field’s ‘The Long and the Short of It’ report tomorrow, complaining about underinvestment in brand. Well, you get what you ask for.

Fifth, the performance claim is vastly overstated. Everybody knows even hard outcomes like conversions rarely trace cleanly back to a single campaign. Someone sees an ad. Later they search. Then they click. Sophisticated attribution exists. Almost no one applies it rigorously. Yet performance marketing implies a direct causal line that rarely holds true.

Finally, the belief locks companies into a vicious spending loop. Budgets flow disproportionately into digital. Returns decay. Meanwhile, you see more outdoor ads for Google and Meta’s performance platforms than for many consumer brands. A generation taught that performance marketing equals ‘right’ marketing follows the script. Bob Liodice, CEO of the American Association of Advertisers, once put a number on it: only 25% of digital media investment reaches target audiences. More than $20bn in marketing waste. So much for performance.

I could add more reasons. But I made my point. There is no sensible justification for the term ‘performance marketing’.

This isn’t a critique of the many good people who carry the performance management title. Many didn’t choose it. Titles get assigned. Job ads get written. Careers get built inside the language available at the time. Performance marketing spread because it sounded modern, measurable and safe. A hype cycle did the rest.

At home, we stopped doing Christmas presents years ago. The hunt for the perfect gift got out of hand. This year, I have one wish. A large box under the tree. Neatly wrapped. On the label: “Performance Marketing.”

I pull the ribbon. The lid lifts. And the whole thing collapses into dust. When it settles, only one word remains: Marketing.

Merry Christmas.

What Amazon’s 14,000 layoffs reveal about AI’s grip on marketing

Amazon’s decision to cut 14,000 jobs this quarter – roughly half the number initially feared – confirms what most boardrooms already know: artificial intelligence isn’t just a productivity tool, it’s a restructuring driver.

Forget the polite language about “culture” from CEO Andy Jassy or “people and customers” from HR chief Beth Galetti. The driver is efficiency. Investors want AI-level margins, not human-level headcount.

And Amazon isn’t the outlier. Nestlé plans to remove 12,000 white-collar roles over the next two years. Salesforce has already replaced 4,000 customer people with the rise of AI agents. UPS has shed nearly 50,000 jobs since 2024, citing machine learning. Agency Dentsu has trimmed 3,400 worldwide. Not all job losses are liked to AI or marketing – but many are.

Check your LinkedIn feed and you’ll see the fallout: marketers, analysts, planners – ‘open to work’.

The pattern is clear. AI is collapsing the space between strategy and execution – the white-collar layer where much of marketing, operations and customer service used to live.

5 marketing jobs already under pressure

SEO. The search-optimisation industry – worth billions globally – exists largely to please algorithms, not customers. As users move from classic search to AI search with Perplexity, ChatGPT and Claude, traditional SEO will fade. It’ll be replaced by a new layer of ‘generative engine optimisation’ (GEO) equally detached from customer value, perhaps just more automated.

Social media management. Posting, scheduling and A/B testing across Meta and TikTok are already automatable. The ‘digital native’ roles created in the 2010s – once seen as the new frontier – are now the first to go. The irony: the generation that disrupted traditional marketing is now being disrupted by its own tools.

Content creation. Routine copywriting and influencer work are being commoditised fast. Virtual influencers have already fronted campaigns for beauty brands like L’Oréal offering perpetual, low-cost exposure – without mood swings, agents or scheduling conflicts. The majority of consumers cannot tell – or do not care – that the presenter isn’t human.

Ad production. Coca-Cola’s first AI-generated classic Coke caravan holiday commercial marked a turning point. Writing on X, Gravity Falls creator Alex Hirsch captured the industry’s unease: “FUN FACT: @CocaCola is ‘red’ because it’s made from the blood of out-of-work artists!” The Verge, meanwhile, described Coke’s latest 2025 AI Christmas ads as “a sloppy eyesore”.

But it’s early days and the shift is inevitable. I once flew 30 people to South Africa for 30 seconds of beach footage. If AI can render 50 versions of the same ad overnight, be my guest. Mondelez just spent $40m on generative video platforms promising to halve production costs. In that kind of math, efficiency always wins the budget battle.

Marketing analytics. Good news. AI may bring rigour to an area marketers have long avoided: measurement. The excuse that “it’s too complex to track” is eroding. AI-driven attribution and modelling could finally give the industry what it has lacked for decades – a standardised way to diagnose growth and prove ROI. For a discipline often allergic to evidence, there’s a cultural reset coming.

The real issue: relevance

I’ve read 20 corporate layoff memos this quarter. Beyond AI, they all mention “less critical roles” and “unnecessary layers”.

Context matters. European GDP (the UK included) will grow just over 1% this year; the US a tad more. Across most markets, budgets are tightening. In that climate, CEOs are asking one question with increasing regularity: does this role contribute to growth?

If the answer is unclear, the role is at risk.

I’ve said it for years – if marketers don’t stand for growth, they stand for nothing. Growth is the reason marketing exists. Yet large parts of the discipline still retreat into comfortable abstractions of ‘brand love’ and ‘storytelling’. In a world where CEOs get more serious about growth, those arguments won’t survive the meeting.

Staying relevant in the AI age: Try this

Look at your role like a CEO

Ask: what are my company’s top three priorities? What are my customers’ top three priorities? The overlap is where growth happens. That’s the value creation zone.

Maybe a competitor has a better product. Maybe your pricing’s off. Maybe your media strategy is underpowered. Whatever your job description says, if you operate inside the value creation zone – and make that visible – your role will be relevant.

Audit yourself

Which parts of your job could AI do better or cheaper? If large chunks can be automated, they will be. You can’t out-AI AI. Replace yourself before someone else does. Let machines handle the routine while you trade up to what they still can’t do well: judgment, creativity and the courage to ask questions no dataset can answer.

Rediscover the creative leader in you

AI will add mediocrity – at scale. Boston Consulting Group ran a revealing experiment: two groups solved the same marketing problems; one using AI, one without. AI helped the group perform 40% better in a product innovation task but resulted in 41% less diversity of ideas. Machines replicate knowledge; they can’t generate intuition. AI makes average things for average people (hello, Mico). Great marketers work on the edges – where ideas still feel slightly dangerous.

The choice ahead

Very soon, every marketer will face their own ‘Matrix moment’ – accept automation’s illusion of control, or take back the job of creating growth. Here’s the choice:

Take the blue pill, and hand over your marketing to the machines (Meta and co are building that version of the future). Take the red pill, and step up as a growth leader who uses AI as leverage.

The choice is existential. In the AI economy, marketing rainmakers stay. Everyone else may become optional.

(From my Marketing Week column).

Why people buy: three lessons from a market research meltdown

The oldest—and hardest—marketing research question is: “Why do people buy?”

Most people simply delegate the answer—feeding a US $140 billion research industry (ESOMAR).

The problem? Many results are skewed, unreliable, or plain wrong.

I learned that the hard way.

Recently, I ran a large global growth leadership study—a classic “driver analysis” that promises to reveal what really moves revenue.

Top agency. Thousands of respondents. 60+ countries.

The report looked fine.

It just didn’t make sense.

So I asked my friend Frank Buckler—who runs a boutique research firm—to run a neural network analysis.

The results flipped. Completely.

A key variable’s importance shifted from +9 percent to −2 percent.

Drivers that came out irrelevant shot to the top.

Marketing has a serious research problem.

So I spoke to several CMOs and researchers about why we still get growth leadership research so wrong.

Here’s what I learned.

Lesson 1: Learn how the growth leadership math works.

Ice-cream sales and drowning deaths rise at the same time.

The correlation is almost perfect.

Does that mean ice cream kills people? Of course not.

When it’s hot, more people buy ice cream—and more people go swimming.

Correlation and cause are different.

Yet many marketers still use correlation as proof of success.

Traditional regression has flaws too.

It assumes something like: “Y changes by a constant amount when X changes by one unit.”

It’s a straight-line world.

We all know that’s nonsense.

Neural networks aren’t perfect, but they’re closer to how real decisions happen.

They don’t assume anything is linear.

They learn patterns directly from data—whether those patterns are straight, curved, or tangled like spaghetti.

You don’t need to become a statistician.

You can google most of this.

But you need to ask the right growth leadership questions—or you may end up with expensive nonsense.

Lesson 2: Treat researchers like peers, not suppliers.

Many researchers are super smart. They would love to have a peer-level debate.

In reality, most get asked for “quick analysis,” and rarely see what happens to their work.

That kills curiosity.

It keeps the same old methods alive.

Take ad tracking.

System1 does one of the world’s best ad-performance measurements.

It doesn’t mean people jump on it.

Insecure analysts stick to what’s safe.

This trickles down to agencies.

The whole system repeats itself: mediocre growth leadership insight, mediocre growth.

Lesson 3: Trust your gut, not the logo.

When my first results came back, I could have accepted them.

Big agency name.

Credibility guaranteed.

But they didn’t feel right.

So I dug deeper.

The new analysis revealed what the first had missed.

Don’t get me wrong—I’m not blaming the agency.

They’d happily run alternative methodologies.

The problem is that few clients ever ask.

The truth about “why people buy” isn’t simple.

If you’re serious about growth leadership, get your hands dirty.

Research is only as good as the curiosity behind it.

The growth lesson hidden in Apple’s latest launch

Meaningful product tweaks enable incremental sales, and while most managefs don’t influence product, they can gradually change that.

“iPhone 17 Disappointment Triggers $112 Billion Apple Market Value Drop,” the headline read. Apple had just unveiled its new iPhone 17 line-up in trademark Cupertino style: slick videos, funky music, Tim Cook and team gliding on camera outside Apple’s glass-and-steel HQ – polished, but a little staged.

But even the best stagecraft couldn’t hide it: Apple missed AI.

Everywhere in tech, AI is the story. AI on the iPhone? It’s hit-or-miss – more miss than hit. Apple did the right thing by not mentioning it. Instead: better cameras, brighter screens, faster charging. And the star of the night: a slightly thinner iPhone Air.

Nice stuff – but not enough to thrill reviewers.

Customers couldn’t care less about what the experts said.

Pre-orders shot up. Analyst Ming-Chi Kuo reported Q3 iPhone 17 production targets were 25% higher than for the iPhone 16 a year earlier. In China, Apple Store slots sold out in minutes. And that $112bn “loss in market value”? Within days, the stock had bounced back. It’s early days and numbers may shift, but the start was stunning.

Apple had done it again: it made the iPhone just slightly better.

Portfolio power

Many marketers still underestimate Apple’s playbook:

Constantly improving stuff: In Simply Better, former London Business School professor Patrick Barwise and Sean Meehan show how great brands thrive not by flashy reinvention but by serving customers “profitably better than competitors do”. Both observed hundreds of companies worldwide. The most successful applied the Simply Better principle: small upgrades, year after year. Marginal in the lab, meaningful in the market.

Tapping into growing segments: iPhone revenues have been flat at around $200bn since 2022 – remarkable given the brutal competition. Services, meanwhile, have soared from $78bn in 2022 to $92bn last year, nearly 18% growth on the back of music, video and apps. My former McKinsey colleagues ran some revealing numbers. Tracking 416 companies for more than a decade, they found just 22% of growth came from market share gains. More came from M&A – 35%. The single biggest driver, at 43%, was portfolio momentum: the sectors, regions and segments you’re in. That’s where growth hides.

Apple plays both sides. It defends and builds. It keeps the iPhone alive with steady improvements. And it finds growth in adjacencies. That’s how you last.

Coffee beats lobster

To see the power of product, look at Tim Hortons and Red Lobster. Two chains. Same problem. Very different outcomes.

Canadians love Tim Hortons. The chain is a cultural icon.

But customers had drifted away – fed up with mediocre coffee and sandwiches. Rivals were using fresh eggs while Tim’s stuck with frozen patties. Revenues were dropping. The core was broken.

Hope Bagozzi, the new CMO, pushed beyond comms to influence the product. She piloted fresh coffee and fresh eggs. Customers raved. But Tim Hortons is a franchise system. The ‘right answer’ wasn’t enough. Franchisees had to agree. Many rounds of persuasion later, the network signed off. The upgrade worked. Customers returned. Revenues rose. Tim Hortons won back its core. Better product. Better experience.

Red Lobster went the other way. The seafood chain’s customer base was aging fast. Young customers shunned Red Lobster. Investors had stripped assets and loaded debt. Restaurants were tired. Then fish producer Thai Union bought control. On paper, it made sense: own the supply, own the restaurants.

But instead of fixing the core, management doubled down on gimmicks. They took a promotion – $20 ‘Ultimate Endless Shrimp’ – and made it permanent. Bargain-hunters flooded in. Overworked staff couldn’t cope. The core didn’t improve. Costs spiralled out of control. Eventually, Red Lobster filed for Chapter 11 bankruptcy protection.

The difference is night and day. Tim Hortons fixed the core product. Red Lobster papered over cracks. One grows. The other dies.

Marketers aren’t where the action is

Tweaking the product is the most powerful growth lever marketers have. It’s how Apple keeps the iPhone alive in a flat market. It’s how Colgate sells toothpaste year after year with tiny but meaningful upgrades. It’s how Dr Martens grew after switching from ‘storytelling’ to product marketing.

Here’s the uncomfortable truth. Most marketers aren’t involved.

Marketing Week’s latest Career & Salary Survey shows 89% of marketers control comms, 79% manage research and insights. Product, service, innovation? Just 49%. A global McKinsey study is more pessimistic: only 38% of marketers had product management responsibility.

Read that again. Less than half of all marketers are meaningfully involved in the thing customers actually buy.

That’s the gap.

Marketers didn’t suddenly ‘lose’ control of the product. In fast-moving consumer goods (FMCG), they always had it. That’s how the profession was built: at Unilever, P&G, Colgate, the brand manager is the product manager. But FMCG is just one corner of the business world. Most marketers don’t work there. They work in services, tech, finance, B2B – places where product has always been owned elsewhere.

Yet, marketers play a role in the low influence on the product.

Think about it, CEOs ask marketers to do one thing: grow the business. Yet if you go to Cannes, you’d think growth means slogans, storytelling, TikTok stunts. Cannes is fun. But growth comes from getting the core offer right. Marks & Spencer, Marketing Week’s Brand of the Year in 2024, proved it. Profits jumped 22% last year. Not just from the (very good) Christmas ads. From revamping food and fashion, sharpening pricing, investing in better stores.

Product and promotion are twins. One without the other is a ghost.

Apple, at least, could never have story-told its way to growth.

Try this

Product ownership won’t flip overnight. Google won’t hand its code to marketing. Maersk won’t let marketers design container ships. But if you don’t own the product, you can still shape it. From years of working with CMOs, here’s what works in practice:

- Start small: Every marketer has one unfair advantage – the voice of the customer. Collect it. Not just feedback, but ideas. Track competitor moves, listen for tiny frustrations, capture the sparks of innovation. Build your own view of how good the product really is – and where it could be better.

- Bring the customer truths into the room: Don’t wait for a big stage. Share them in one-on-ones, in hallway chats – and, later, in meetings where nobody expects the marketing voice to show up. At first, it feels risky. Over time, it builds presence.

- Once you’ve earned a little standing, step up: Champion the upgrade that makes a customer smile. Fight for the small detail that keeps people loyal. Show, like the marketers at Tim Hortons, that you can add real value.

If you call yourself a marketer, no matter what your job description reads, don’t stay on the sidelines of product. You know customers. You have insights nobody else has. Get in there. You can do this.

And always remember: no ad will save a poor offer.

(From my Marketing Week column)

Japanese version for Nikkei is here

Take the Growth Leader Test

Are you a growth leader? Take the research-based assessment to see how you lead for growth—and where to lead better.

Growth leaders are different. They drive measurable business expansion. They IGNITE growth through openness and creativity, RALLY people through strategic alignment, and DARE to act when others hesitate in uncertainty.

The question is: do you have the behavioral patterns of a proven growth leader?

Take the brand new 2-minute research-backed assessment to discover your growth leadership profile across the three dimensions that consistently drive business results.

Take the Growth Leader Test now

How the Growth Leader Test Came to Life

This brief growth leadership assessment is based on behavioral data from over 3,000 business leaders across 50+ countries. We measured specific growth leader patterns against real business outcomes—revenue expansion, market share growth, team performance, and organizational influence. The three dimensions consistently separated high-growth leaders from traditional managers across every business metric we tracked.

This quick assessment gives you an initial snapshot of how your leadership style aligns with proven growth leader behaviors. It’s designed as a rapid indicator, not a comprehensive evaluation—think of it as a starting point for understanding your growth leadership potential.